")

Table of Contents

gorodenkoff

In this article I will provide a glance into Amazon (NASDAQ:AMZN) from the United States and Alibaba (NYSE:BABA) from China from a purely fundamental viewpoint. BABA and AMZN are two of the most significant e-commerce corporations in the globe and the largest cloud computing vendors in their respective domestic markets. I believe that both corporations are undervalued and existing a very long-time period financial investment possibility, primarily based on fundamentals.

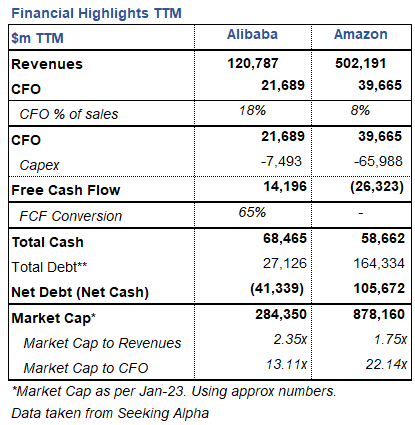

Please discover down below a comparison of the companies´ monetary metrics throughout the trailing twelve months:

Amazon & Alibaba Monetary Highlights (Looking for Alpha)

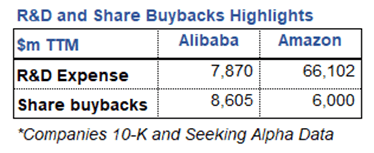

As presented in my prior write-up about Meta Platforms (META) and Tencent (OTCPK:TCEHY) as perfectly as in the short article about Baidu (BIDU) and Alphabet (GOOG) (GOOGL), I also consider a seem at R&D commit and share buybacks. It is essential to look how considerably BABA and AMZN are investing in innovation and their platforms as very well as how significantly they are investing to repurchase their popular inventory and lower the range shares of remarkable in the open up current market. Vital to be aware listed here that equally companies have noticed their price drastically decrease throughout 2022.

R&D and Share Buybacks highlights (Searching for Alpha)

Examining AMZN and BABA Fundamentals and Advancement Probable

AMZN

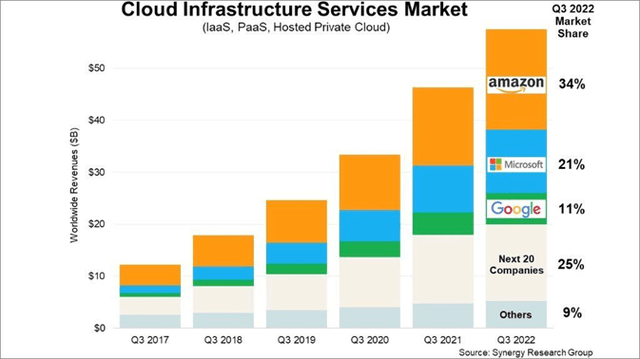

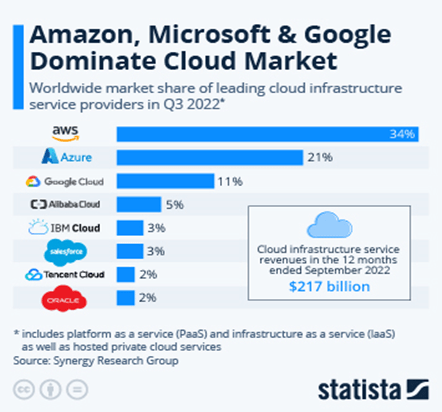

As we all know AMZN is the greatest e-commerce business in the United States and the top cloud computing participant in the entire world. The corporation has noticed a drop in its marketplace valuation because it experienced its eyes set at $2 trillion, the fall has been significant and is now investing at a market valuation of $878 billion. AMZN is able to generate a powerful income stream from functions at $40 billion which during the very last twelve months the corporation had to expend buying property and machines which has now ballooned to $66 billion throughout the past twelve months. AMZN has normally invested its methods to experience positive aspects at a later on phase, we can just acquire a glance at its AWS company, which has above 30% market place share in the worldwide cloud sector. This market place has now surpassed the $200 billion mark during 2022.

Cloud Marketplace (Synergy Exploration Group)

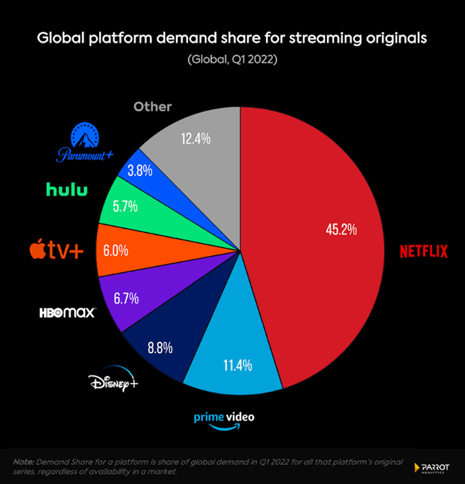

Another case in point of AMZN expense system is its R&D shell out which is substantially higher than most tech companies. AMZN expended a whopping $66 billion in R&D costs throughout the past twelve months. It is for the reason that of this financial investment frame of mind of the management that AMZN has a dominant posture in the e-commerce, cloud computing, and video streaming marketplaces. AMZN is now generating solid investments and seeking to become a dominant player in other industry these types of as the on-demand streaming solutions industry which is forecasted to achieve the $330 billion mark by 2030.

World wide Platform Need Share (Parrot)

Essentially, AMZN has very powerful financials with enormous TTM revenues of $502 billion, a complete dollars posture of $59 billion, and a sturdy funds stream from operations. AMZN does have significant personal debt but let´s not forget that this is primarily due to the fact of working leases. Primarily based on the present-day valuation of $878 billion and the firm’s strong marketplace situation in e-commerce, cloud computing, and video clip streaming, it is very likely that we will see the firm’s valuation return to its 2021 concentrations. The cloud computing marketplace is projected to attain $1.2 trillion by 2027, and the on-demand from customers streaming providers market is anticipated to increase to $330 billion by 2030. With a dominant existence in these marketplaces and in e-commerce, the enterprise is effectively-positioned to encounter significant profits and gain progress. Overall, AMZN has proven it can diversify away from its most important earnings section, which has authorized the business to come across financially rewarding prospects. We can anticipate administration will keep hunting for and finding alternatives which will established the company for very long expression price creation.

BABA

BABA has experienced a steep drop in its industry valuation throughout the final two a long time, with headwinds coming from all instructions. Chinese Regulators have punished the enterprise through fines, blocked IPO, and so forth. These events have impacted investor sentiment and has manufactured buyers wary about the potential clients of the corporation. Having said that, buyers really should note that organizations from the United states of america also undergo and have endured scrutiny from the U.S. or European regulators. Let´s not ignore about Microsoft´s (MSFT) high-quality in 2004 by EU regulators or a lot more not too long ago META´s high-quality by EU regulators for approx. $400 million.

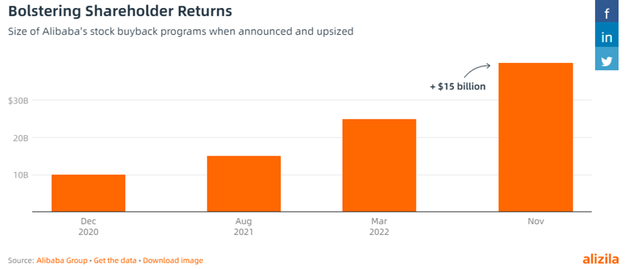

Anyways searching at BABA financials, we can obviously see that regardless of the headwinds the business has been able to produce good benefits. With TTM revenues north of $120 billion and free money flow of $14.2 billion, BABA has more than enough hearth ability to pursue expansion prospects or share buybacks. Management created it obvious it is pursuing share buybacks with the announcement that the company would raise its share buyback method from $25bn to $40bn.

BABA Share Buybacks Improves (Alizila)

BABA is ready to go after this system thanks to its strong equilibrium sheet which is bolstered by its cash posture of $68 billion and web funds situation (funds – credit card debt) of $41 billion. With the existing market capitalization, administration could redeem at least near to 10% of its shares exceptional. On the lookout at BABA hard cash stream to value getting near to 13 periods it presents an appealing opportunity as the corporation still has the opportunity to keep growing. For instance in the cloud field which is set to grow in China by itself to $84 billion by 2027 and globally to $1.2 trillion by 2027. Let´s not forget about that BABA is the major cloud participant in China and major 5 in the globe, which positions the business to consider advantage of this prospect.

As a foremost participant in the e-commerce and cloud computing marketplaces in China, and with a market place valuation under $300 billion, BABA provides an eye-catching long-time period expenditure chance. The company has sizeable room to increase in these markets, and its powerful income circulation from operations enables for intense repurchasing of its common inventory, which will enhance earnings per share. In the prolonged term, we can assume to see an boost in earnings and a lower in share count, ensuing in substantial appreciation of earnings for each share.

World-wide Cloud Marketplace (Synergy Investigate Team)

Risks

Regulatory threats: As pointed out higher than, these companies are matter to quite a few restrictions in their domestic marketplaces as properly as abroad. As it has been noticed all through the several years, fines by regulating entities are not a uncommon event. Some examples to position out are the fines delivered to BABA and TCHEY in China or to META and MSFT in the United states of america and Europe. Greater regulatory scrutiny will surely effects these corporations at some level and this could have destructive repercussions for their monetary general performance.

Geopolitical challenges: It is no mystery that both AMZN and BABA facial area geopolitical risks, the modifying planet order is impacting all organizations in the world. Because of to the large dimension of these companies’ political instability, trade disputes, and other impactful occasions could hinder their functions and monetary effectiveness.

Conclusion

AMZN and BABA are both substantial influential firms in the tech business. AMZN is the leading e-commerce organization and cloud computing participant in the United States, though BABA retains the very same top posture in China. Nevertheless, BABA has faced a number of headwinds in modern quarters, which includes fines and regulatory troubles in China and this has led to a sizeable decline in its market valuation. Overall, both of those AMZN and BABA have quite potent fundamentals and the potential for foreseeable future growth in marketplaces which are set to improve in benefit noticeably all through the next several years.

Editor’s Take note: This report discusses one or additional securities that do not trade on a main U.S. trade. Be sure to be conscious of the risks related with these stocks.

More Stories

What Are The Types of Magento Hosting Services

User Experience (Ux) Design Strategies For E-Commerce Sites

TikTok is wading into South-East Asia’s e-commerce wars