Table of Contents

E-commerce shares have taken quite a few methods again above the past calendar year as tech names from throughout the board took a violent tumble. As shares stabilize, I imagine now could be a fantastic time to go buying for price.

Certainly, a price-induced economic downturn and a potential pullback in buyer paying feel to be on the way. Though individuals have now reacted to significant inflation and a weakening economy, it is tough to explain to just how significantly the battered e-commerce darlings stand to fall as shoppers rein in spending.

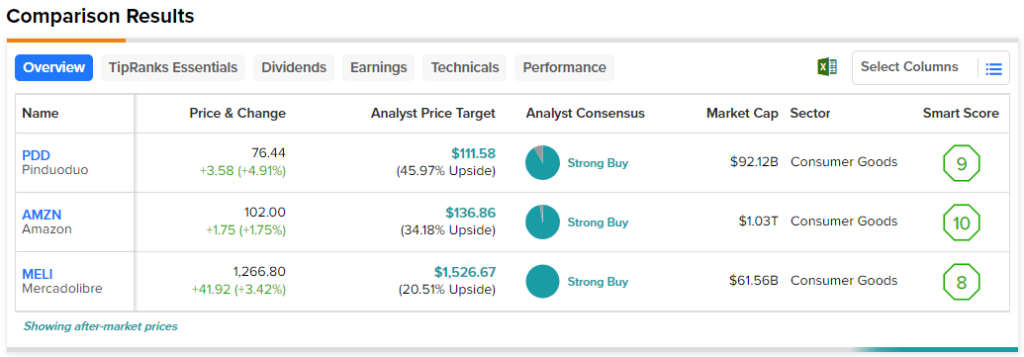

In any case, let us use TipRanks’ Comparison Software to get a glimpse of 3 Solid-Invest in-rated e-commerce plays.

Amazon inventory seems ready to shift on after enduring a 55% peak-to-trough fall. An overinvestment in potential, macro headwinds, and rocky management from CEO Andy Jassy may possibly nevertheless be brings about for issue. Irrespective, I continue to see Amazon as 1 of the most impressive and disruptive corporations out there. With layoffs and other charge cuts in the rearview, I think Amazon has a great deal of issues it can do to reignite trader enthusiasm yet again, even in the experience of recession headwinds. I am bullish.

Administration offered careful guidance, which, I think, lowers the bar dramatically. With inflation and a economic downturn in the playing cards, it’s firms like Amazon that are likely to just take a spill effectively before it has a opportunity to report actually hideous quantities. Even though Amazon has dissatisfied in earlier quarters, I don’t feel we’ve viewed a thing actually horrific from the company still. I imagine today’s depressed multiples advise that these kinds of a quarter is being priced in.

As Amazon carries on to construct industry share with progressive platforms (believe the all-in-a person Obtain with Key assistance, which “allows US-based Prime users to store specifically from taking part on-line shops employing the Prime shopping rewards they really like and trust”), I’d glance for Amazon to be a person of the leaders the moment the market’s all set to concentrate on an financial recovery.

It is really hard to inform wherever Amazon goes from here. A recession has not even strike yet. AWS and retail revenue could simply proceed to drag their ft. In any circumstance, I locate it really hard to move up the demonstrated innovator though it is investing at 2. instances gross sales, 45% lower than its 5-calendar year average. That’s also very low for a disruptive innovator.

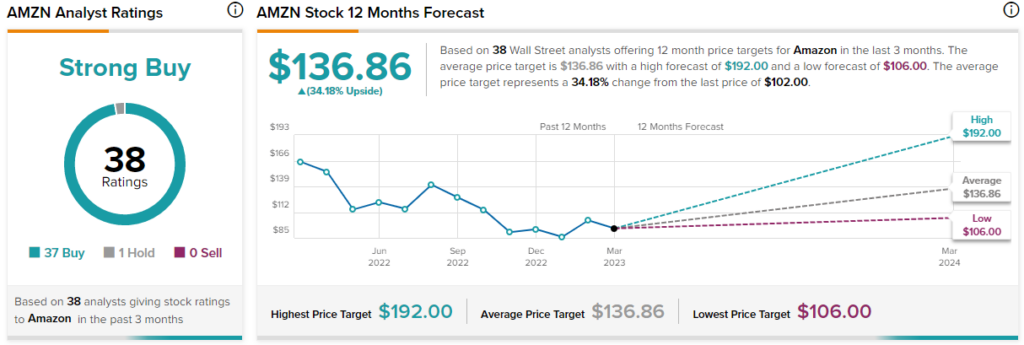

What is the Cost Focus on for AMZN Inventory?

Analysts assume massive matters from the e-commerce behemoth, which stays a Sturdy Purchase with 37 Purchases and just just one Maintain. The regular AMZN stock rate goal of $136.86 implies 34.2% upside opportunity.

MercadoLibre is an e-commerce enterprise that operates in Latin The usa. It is essentially the Amazon for a variety of international locations in the Latin American location. Like Amazon, MercadoLibre’s arrive at goes nicely over and above just digital gross sales. The firm has a monetary business (payments and lending), a strong advert small business, and a logistics division (Mercado Envios). With a extensive expansion runway and a dominant presence in Latin America, I am bullish.

Without doubt, macroeconomic headwinds have weighed across all elements of the world. Continue to, in its most current quarter (Q4), MercadoLibre posted some impressive outcomes, with for each-share earnings of $3.25, perfectly forward of the $2.42 estimate. Thus, even as shoppers felt the pinch of a slowing overall economy, the organization managed to electrical power enviable progress premiums, many thanks in portion to its financial providers and advertisements.

In truth, there are even now a lot of possibilities to transition consumers absent from employing money. As a result, as spectacular as the $65 billion e-commerce agency is with its on the internet marketplace, it is the fintech small business that could assist jolt growth and pad margins.

Seeking forward, MercadoLibre however appears to have its foot on the pedal. The firm is slated to make investments $1.6 billion in Mexico this year into enhancing its e-commerce abilities, monetary expert services, and logistics. The money will also go toward advertising.

At 72.5 times ahead earnings, MELI inventory nonetheless seems costly even although shares are off 37% from their highs. Even so, the inventory is a large amount more affordable from a historic perspective. MercadoLibre has commanded rate-to-earnings (P/E) multiples in the hundreds in the previous. You have to fork out up for expansion. At these amounts, I really do not consider buyers are shelling out up all too substantially, at the very least traditionally talking. Analysts concur.

What is the Price Concentrate on for MELI Stock?

Wall Avenue loves MercadoLibre, with a Robust Obtain rating primarily based on nine unanimous Obtain ratings. The regular MELI inventory price goal of $1,526.67 involves a 20.5% attain from below.

PDD Holdings is a Chinese e-commerce organization that took the toughest hit of the names in this piece. At its worst, shares crumbled just about 89%. Shares finally recovered but are now back in retreat mode, now down nearly 30% from 52-7 days highs. While the hottest quarter was worrisome, I stay bullish.

Shares took a 14% strike when PDD disclosed disappointing fourth-quarter final results. The operator of Pinduoduo and Temu skipped on earnings ($5.77 billion vs. $6.025 billion estimate) and posted a slight miss on per-share earnings ($1.21 vs. $1.22 estimate). Moving forward, PDD inventory is most likely to be a pretty choppy roller-coaster trip as the Chinese economic restoration proceeds dragging out.

At 22.9 situations trailing cost-to-earnings with stable advancement forward (analysts count on 28% income growth this year), PDD Holdings may really very well be the most effective deal of the batch. Nonetheless, there are included risks to investing in Chinese stocks. Most notably, delisting is a issue typical in any U.S.-listed Chinese inventory. Although it is difficult to gauge stated threats, I believe these cozy with bearing them could have a shot at an outsized reward.

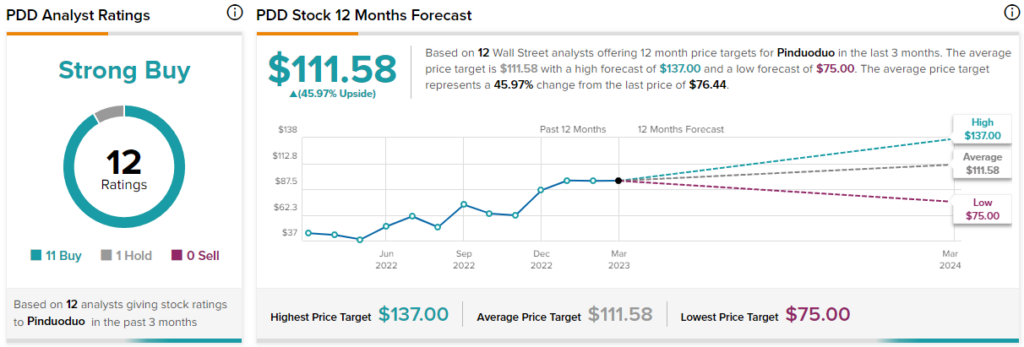

What is the Price tag Concentrate on for PDD Inventory?

Analysts have a Powerful Invest in rating on PDD, with 11 Purchases and a single Maintain. The common PDD stock selling price concentrate on of $111.58 indicates 46% upside opportunity.

Summary

If the Fed can accomplish its mission (I assume that’s a likely state of affairs) and orchestrate a delicate landing for the economy, then the recession danger baked into e-commerce performs may well be overblown. With current regional financial institution failures, the Fed might not want to raise costs as a great deal as originally anticipated, which could bode properly for stocks.

Disclosure

More Stories

What Are The Types of Magento Hosting Services

User Experience (Ux) Design Strategies For E-Commerce Sites

TikTok is wading into South-East Asia’s e-commerce wars