Table of Contents

oatawa

MercadoLibre (NASDAQ:MELI) continues to trade well below all-time highs in spite of continued strong financial results. The “Amazon of Latin America” has generated solid growth in spite of reopenings as the juggernaut continues to take market share. The fintech business segment is still growing at incredible rates, and the company has pulled back on loan originations amidst a tough macro environment. This is a stock that has traditionally traded at very rich valuations, but after the past few years of meteoric growth coupled with the plunge from recent highs, the stock is now offering a rare opportunity to buy high quality at a great price. Stay long here – I continue to rate MELI a strong buy for long-term investors.

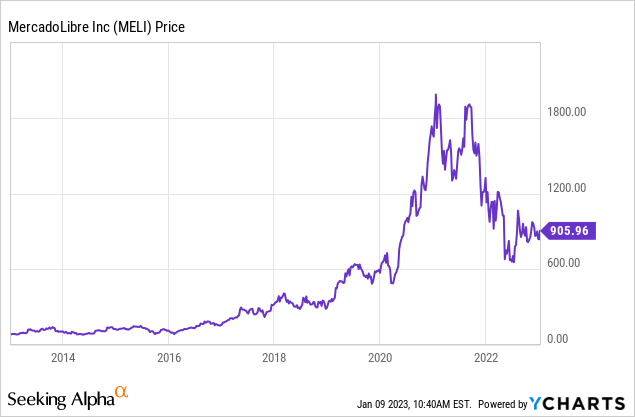

MELI Stock Price

MELI has crashed since reaching $2000 per share in early 2021.

I last covered MELI in October where I rated the stock a buy on account of the strong growth, solid margins, and reasonable valuation. Those factors have not yet changed, and MELI continues to execute strongly even as macro conditions worsen.

MELI Stock Key Metrics

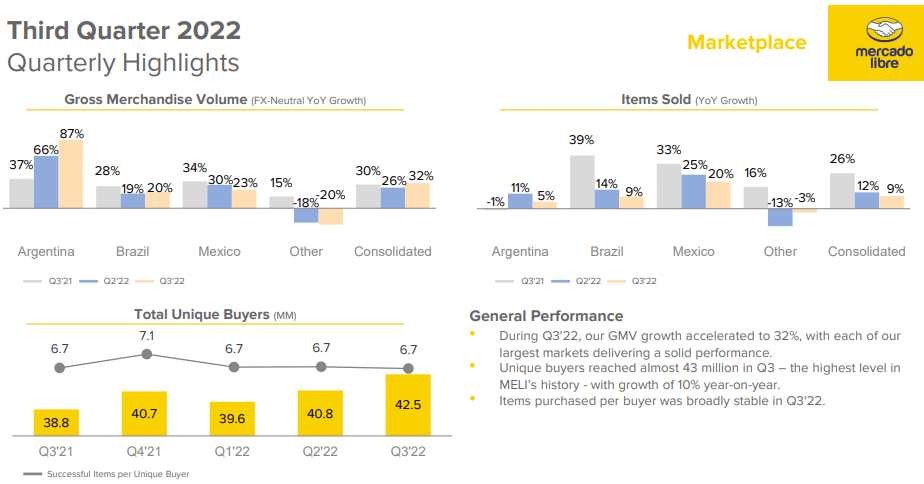

The latest quarter saw MELI deliver 32% growth in GMV – an incredible feat considering that the company grew GMV by 30% in the same quarter of 2021.

2022 Q3 Presentation

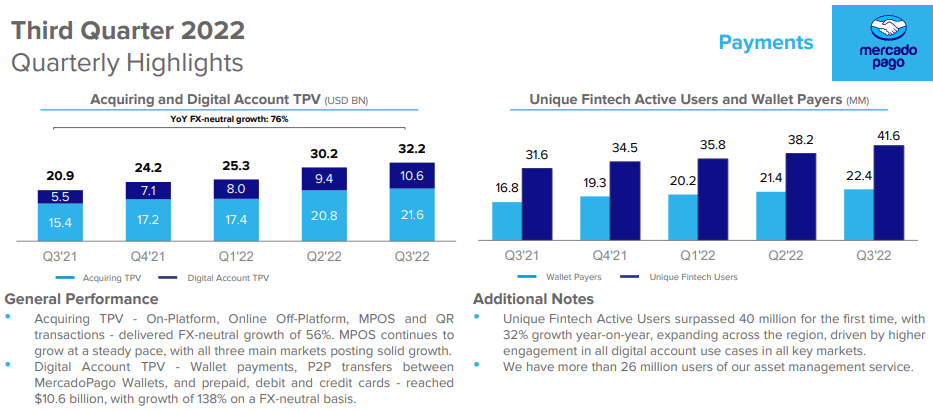

That’s already impressive growth, but the fintech side of the business was the real star, with total payment volume growing 76% YOY.

2022 Q3 Presentation

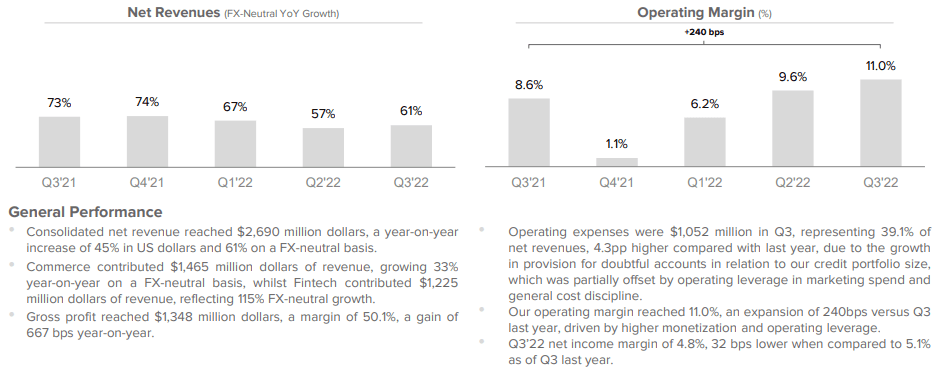

The huge growth in fintech operations helped overall revenues grow by 61%. While that represents some deceleration from the 73% growth of the prior year, I doubt many investors will complain, considering that many e-commerce peers are generating muted growth due to tough comps. Meanwhile, operating margins expanded meaningfully to 11% as the company benefited from operating leverage. This is not a situation where you need to choose between either high revenue growth or high profits.

2022 Q3 Presentation

We can see below that MELI generated its strongest growth from its core markets.

2022 Q3 Presentation

The only business segment that faced road bumps was that of the credit portfolio. As stated in the shareholder letter, the company “took a deliberate decision to slow originations” as they recognized the risks associated with a weakening lending environment. Management viewed this as a short-term roadblock, emphasizing on the conference call that they are not aiming to build a large loan book as fast as possible, but instead one that is sustainable and profitable over the long term.

2022 Q3 Presentation

MELI did see a sharp jump in loans 90 days past due – management noted that this was due to the slowdown in originations as previous loan cohorts kept aging.

2022 Q3 Presentation

Further, as can be seen above, there was some sequential decline in provision coverage. Management noted that they are “provisioning pretty much 93% of all of the loans that are over 90 days past due and over two-thirds, 68% of those that are between 1 and 90 days past due.” My view as a shareholder is that the credit portfolio still has sizable work to do in terms of improving underwriting standards and margins.

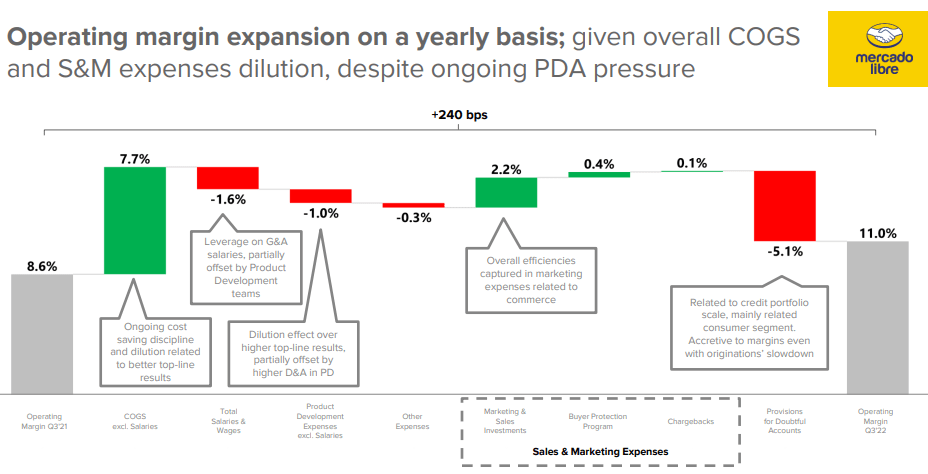

I stated above that MELI was able to drive meaningful operating leverage in the quarter. As can be expected due to the large e-commerce presence, MELI benefited from increased scale, but the credit portfolio continued to drag meaningfully on results.

2022 Q3 Presentation

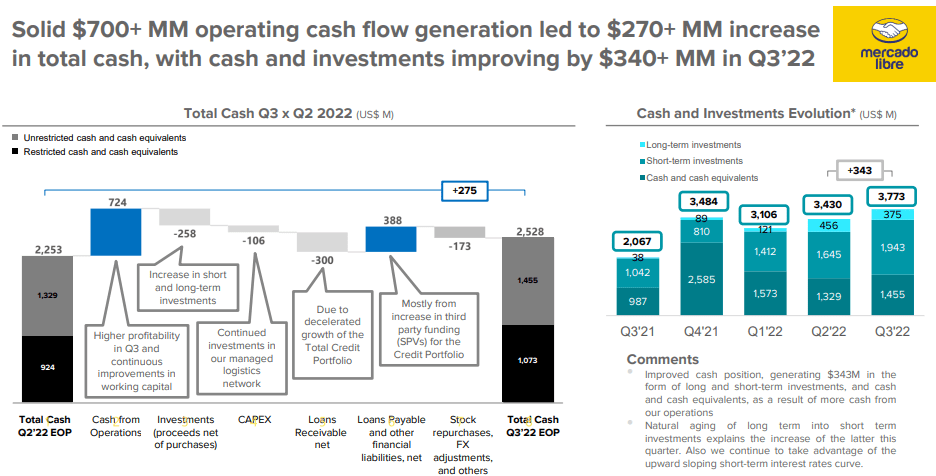

MELI continued to generate meaningful cash. Free cash flow stood at $618 million. After accounting for investments and other items, the cash balance increased by $275 million.

2022 Q3 Presentation

MELI ended the quarter with $3.8 billion of cash and investments, $4.6 billion in debt, $2.6 billion of credit card receivables, and $1.1 billion of restricted cash. It appears that even in a doomsday scenario, MELI has enough net cash to fully cover any losses in its credit portfolio.

Looking forward, management expects stronger margins in the fourth quarter. While the company typically is very aggressive on the promotional front in the quarter (as evidenced by the lower margins in the fourth quarter of 2021), management expects its stronger first-party business to allow it to post stronger margins than the prior year.

Is MELI Stock A Buy, Sell, Or Hold?

At recent prices, MELI was trading at just around 4x sales. This is a stock that has historically traded at double-digit price to sales multiples.

Seeking Alpha

Assuming 20% long-term net margins, 25% growth, and a 1.5x price-to-earnings growth ratio (‘PEG ratio’), I estimate the fair value of MELI to be around 7.5x sales, or $1580 per share. I find that 20% long-term net margin target to be conservative, considering that MELI is already generating double-digit operating margins. As the higher margin fintech business continues to grow rapidly and the company benefits from operating leverage in e-commerce, I expect profits to grow meaningfully faster than the top line.

There are many risks to consider here.

As I stated in my prior report, inflation and interest rates are significantly higher in Latin America than in the United States. Argentina, MELI’s home country, raised its interest rate to 75% in September and has since kept it at that rate. With interest rates so high, one can be forgiven for feeling like there may be a doomsday scenario on the horizon – MELI stock would undoubtedly be hit hard if that occurs.

Another risk is how pulling back from loan originations will affect marketplace growth. Management previously estimated that credit made up a low-double-digit percentage of marketplace sales. That might suggest minimal impact, but future quarters may show sharp deceleration if that estimate proved incorrect.

At the risk of sounding like a prideful American, MELI possesses international risk. I have already discussed the economic risks from high interest rates – there is also the risk of political uncertainty and in the event of fraud, it is not clear if shareholders would have as much shareholder protections as afforded by domestic companies. Perhaps these may prove to be unsubstantiated fears, but after what we have seen take place with Chinese equities over the past few years, some caution may be warranted.

It is worth noting that Southeast e-commerce giant Sea Limited (SE) announced in September that it was exiting Mexico, Argentina, Chile, and Colombia. That removes one large competitor from MELI’s operating markets and may help boost margins in the near term. As discussed with subscribers to Best of Breed Growth Stocks, investing wide across a variety of quality undervalued tech stocks may be the best way to take advantage of the crash in tech stocks. MELI fits right in with such a basket as the stock is offering high secular growth at more than reasonable valuations.

More Stories

What Are The Types of Magento Hosting Services

User Experience (Ux) Design Strategies For E-Commerce Sites

TikTok is wading into South-East Asia’s e-commerce wars