Current strains at some banks in the United States and Europe are a impressive

reminder of pockets of elevated economical vulnerabilities designed around a long time

of reduced prices, compressed volatility, and sufficient liquidity.

This sort of pitfalls could intensify in coming months amid the continued tightening

of monetary coverage globally, earning it particularly critical to understand

and safeguard this wide swath of the economical sector that includes an

array of institutions over and above financial institutions.

Nonbank economical intermediaries, which includes pension resources, insurers, and hedge funds, also enjoy a important function

in the world monetary process by furnishing economical expert services and credit rating

and so supporting financial progress.

The expansion of the NBFI sector accelerated following the world wide economical

disaster, accounting now for virtually 50 % of world wide monetary property. As

these kinds of, the smooth performing of the nonbank sector is very important for fiscal

stability.

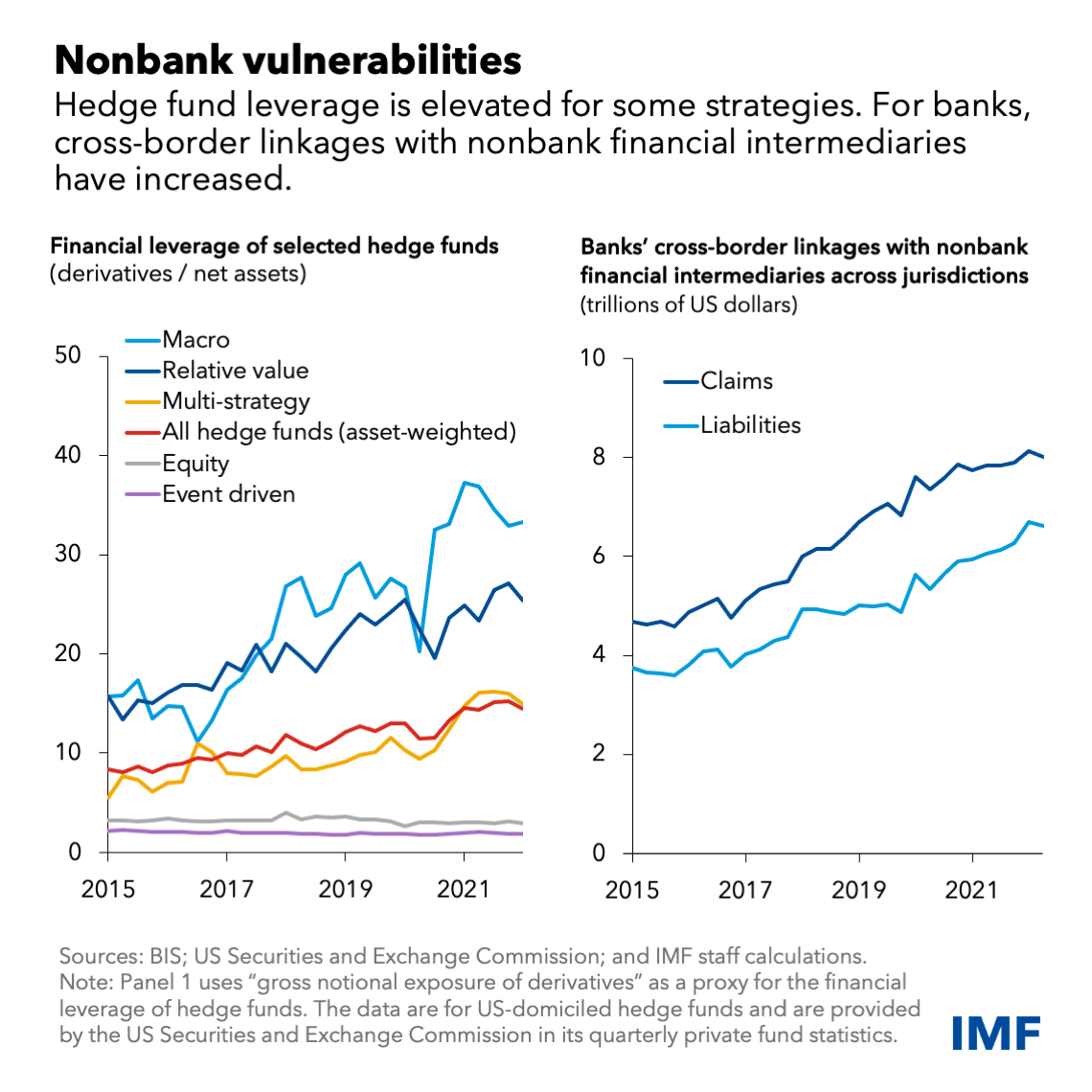

Nevertheless, NBFI vulnerabilities appear to have enhanced in the earlier 10 years.

As we present in an analytical chapter of the latest

World Economic Steadiness Report, NBFI tension tends to emerge alongside elevated leverage, for

example borrowing revenue to finance their investments or increase returns, or

applying financial instruments, like derivatives.

Worry is also brought on by liquidity mismatches, exactly where an

institution is unable to create ample dollars both by means of

liquidation of property, these kinds of as bonds or equities, or use of credit score lines to

satisfy investor redemption requests.

Ultimately, higher degrees of interconnectedness between NBFIs and with

conventional banking institutions can also come to be a essential amplification channel of

fiscal stress.

Previous year’s United kingdom pension fund and liability-pushed expense methods

episode underscores the perilous interaction of leverage, liquidity risk, and

interconnectedness.

Issues about the country’s fiscal outlook led to a sharp increase in British isles

sovereign bond yields that, in transform, led to big losses in

defined-reward pension fund investments that borrowed in opposition to this kind of

collateral, resulting in margin and collateral calls. To meet these phone calls, pension money ended up forced to sell government bonds,

pushing their yields even bigger.

It is helpful to consider a stage back again and seem at the latest atmosphere in

which NBFIs find them selves. With the fastest inflation in a long time, and

with cost steadiness at the core of most central bank mandates, injecting

central bank liquidity for monetary balance functions could complicate

the struggle from inflation. In a minimal-inflation ecosystem, central banking companies

can react to economic anxiety by easing coverage these kinds of as reducing interest

premiums or getting property to restore sector performing.

Amid higher inflation, even so, complicated tradeoffs could emerge for central

banking institutions between fostering financial balance and acquiring price balance

in the course of intervals of pressure that may perhaps threaten the wellness of the money

program.

Policymakers need correct equipment to tackle turmoil in the NBFI sector

that might adversely affect economic stability. Robust surveillance,

regulation, and supervision are necessary pre-requisites. Policymakers have to

also narrow or remove gaps in regulatory reporting of important data,

including how considerably risk corporations are having with their borrowing or use of

derivatives.

Procedures are also essential to make certain NBFIs improved handle pitfalls, and this

might be completed by way of timely and granular community knowledge disclosures

and governance prerequisites. These advancements in non-public sector hazard

management must be supported by suitable prudential standards, which include

funds and liquidity requirements, together with improved resourced and stricter

supervision.

This would enable steer the company choices of the NBFIs on their own absent

from excessive chance using by getting rid of equally the incentive and option

to just take on too much danger. It would also likely decrease the need to have for and

frequency of central financial institution intervention to deliver liquidity help all through

systemic worry activities.

If central bank intervention is necessary, they can think about three broad kinds

of assistance:

-

Discretionary market-extensive intervention

should be short-term and qualified to people NBFI segments posing hazard to

economical stability. The timing is also critical—a framework ought to be

in place where knowledge-pushed metrics result in a potential intervention,

while policymakers eventually retain the discretion to intervene. -

Loan company-of-last-resort intervention

need to be obtainable when a systemically essential nonbank establishment

comes under worry. These kinds of lending ought to be at the discretion of the

central bank, at a higher fascination fee, completely collateralized, and

accompanied by larger supervisory oversight. A very clear timeline should

be recognized for restoring the NBFI’s liquidity and return to current market

finance. -

Obtain to standing lending amenities

could be granted to precise NBFI entities to cut down spillovers to the

financial system, while the bar for such entry must be quite large

to stay clear of moral hazard. Entry need to not be granted with no the

acceptable regulatory and supervisory regimes for the unique sorts

of NBFIs.

Crystal clear communication is crucial, so that liquidity help is not perceived

to be doing the job at cross-uses with monetary coverage. For case in point,

getting belongings to restore economical stability whilst continuing with

quantitative tightening to provide inflation back again to goal may perhaps cloud intent

and complicate interaction. Announcements of central lender liquidity

help need to evidently clarify the money security objectives, software

parameters and timing.

At the exact same time, cooperation amongst domestic policy makers and

international coordination involving countrywide authorities is critical. This

allows greater establish pitfalls and regulate crises. Specifically,

internationally coordinated reforms can lower the risks of cross-border

spillovers, regulatory arbitrage, and current market fragmentation.

Given the developing dimension and intermediation capacity of the NBFI sector

globally, the development of the proper toolbox for accessibility to central bank

liquidity, alongside with the suitable guardrails limiting the require for its

use, is a precedence. The need to have to do so is all that a great deal increased offered that

money sector vulnerabilities could be poised to expand amid the ongoing

tightening of monetary policy.

—This website is based on Chapter 2 of the April 2023 International Economical Stability Report, “Nonbank Monetary Intermediaries: Vulnerabilities Amid Tighter Monetary Disorders.”

More Stories

How to Analyze Financial Markets Using Fundamental and Technical Tools

Arbitrage Opportunities In Financial Markets

Options Trading And Volatility